Short-Term Rental Insurance: The 5-Layer Protection Stack Every Owner Should Understand

ASTRO does not sell insurance, endorse any provider named in this guide, or receive compensation for provider examples. This article is educational only—not insurance, legal, tax, or financial advice. Provider names are research starting points. Insurance carriers offer policies and products; booking platforms offer host protections and platform terms; ASTRO programs (Owners Exchange, AArtners, and related owner surfaces) are separate from insurance coverage.

What owners need to understand before something goes wrong

Short-term rental owners live with a different kind of risk than ordinary homeowners. A guest can damage the property. Someone can get hurt. A reservation can go badly. A platform protection process may not cover what the owner assumes it covers. A homeowner policy may exclude business use. A landlord policy may not fit short-term stays. A direct booking may not carry the same protections as an OTA booking.

By the time an owner discovers the gap, it is usually too late.

Insurance is part of the operating foundation of the property, not an afterthought. The goal is not simply to buy more coverage. The goal is to understand the protection stack around your property, your guests, your bookings, your amenities, and your business—and to know which parts are protected, by whom, under what policy, product, protection process, or platform term, with what exclusions, and with what proof you would need if something went wrong.

The biggest mistake owners make about protection

Many owners assume that if Airbnb or Vrbo offers host protection, the property is covered end to end. Platform protections can help on eligible bookings, but they are not a substitute for a property policy matched to short-term rental use, direct bookings, amenities, and your state. A platform protection process is usually channel-specific and governed by platform terms—not by your declarations page.

Short-term rental risk usually needs a stack

- core short-term rental property insurance;

- liability coverage;

- contents and furnishings coverage;

- business income or loss-of-rents coverage;

- guest damage protection or damage waivers;

- guest screening and identity verification;

- travel insurance or trip protection for guests;

- booking-platform host protections from Airbnb, Vrbo, or another booking channel.

Not every owner needs every layer. Every owner should know what each layer does, what it does not do, and where gaps may exist.

Layer 1: Core short-term rental property insurance

Core STR property insurance is the foundational layer. This is the policy that should address the structure, owner-owned contents, liability exposure, business use, and income interruption, depending on the policy.

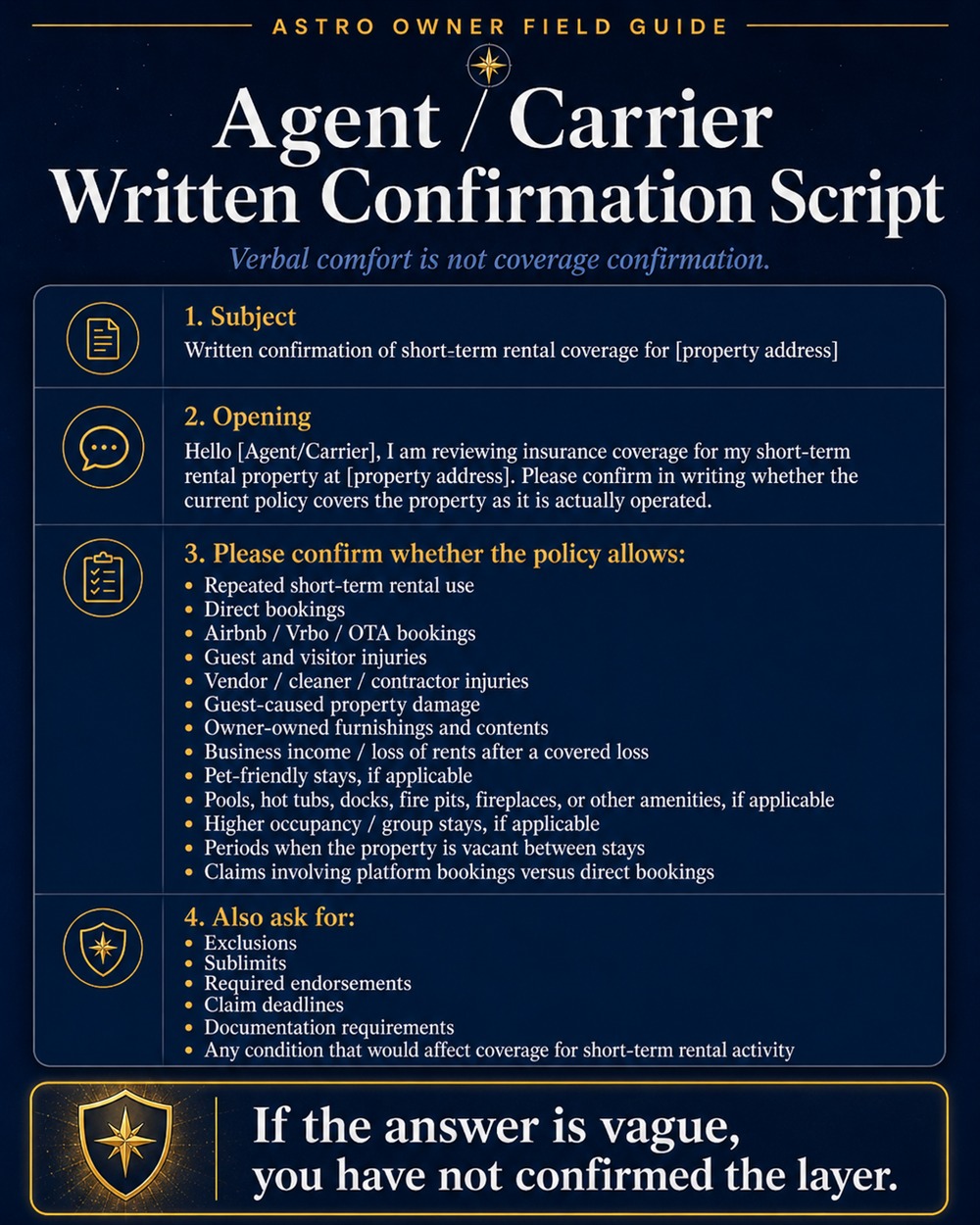

A standard homeowner policy or long-term landlord policy may not be enough for guest turnover, direct bookings, cleaning crews, amenities, and vacancy between stays. Ask your agent or carrier in writing whether your policy clearly allows short-term rental use—not “the platform has coverage,” not “I only rent part-time.”

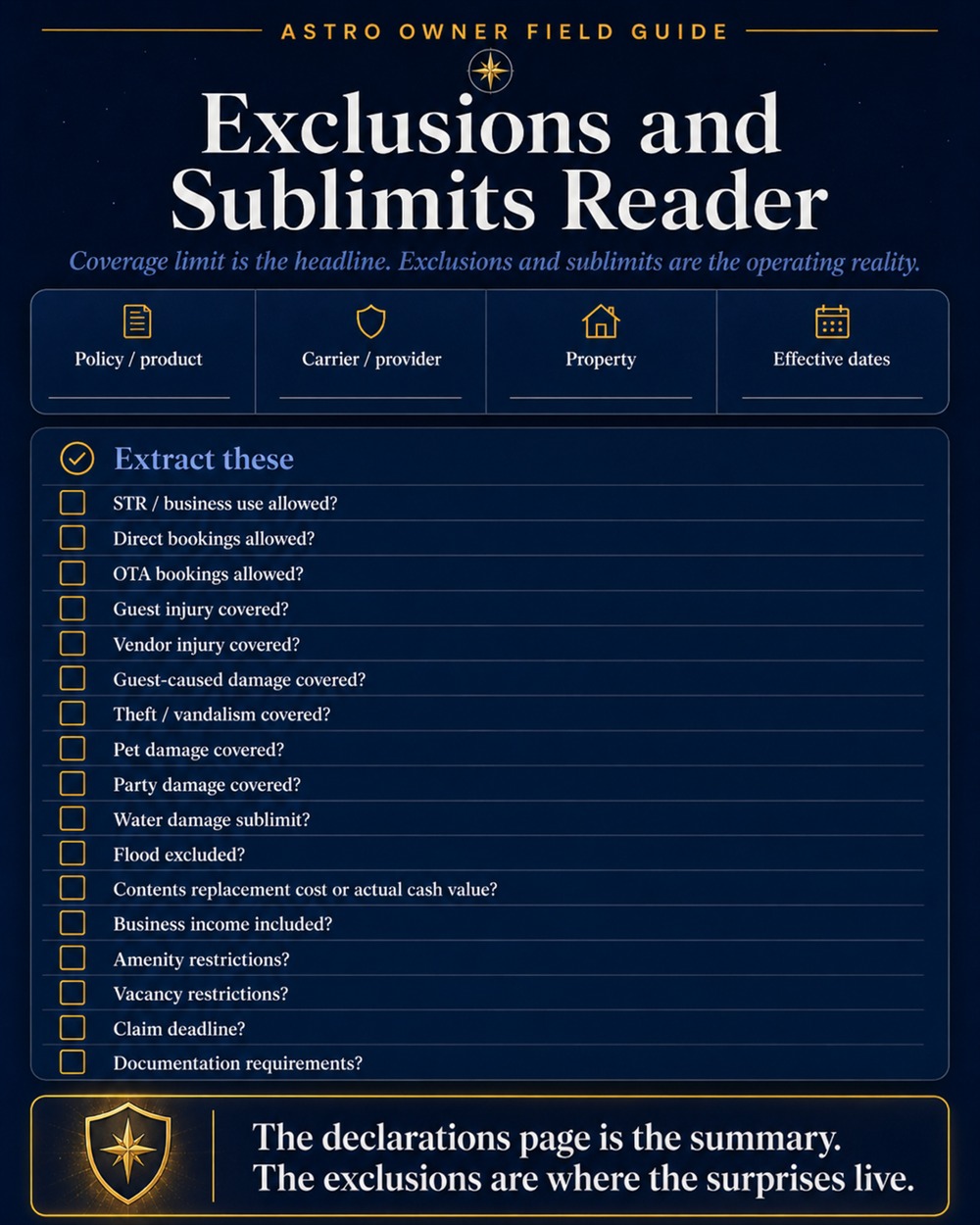

Confirm whether the policy addresses: STR activity; OTA and direct bookings; guest, visitor, and vendor injuries; guest-caused damage; furnishings and contents; business income interruption; cleaning crews and vendors; pools, docks, hot tubs, and similar amenities; pet-friendly stays; local regulatory requirements; claims documentation; deductibles, sublimits, and exclusions.

Layer 2: Guest damage protection and damage waivers

Guest damage protection addresses guest-caused damage during a stay, often per booking. It can help owners avoid treating every broken item, stained rug, damaged wall, or missing object as a major property claim.

Especially relevant for direct bookings, high-turnover properties, furnished homes, pet-friendly stays, and larger group stays.

Some offerings are insurance products. Some are damage waivers. Some are reimbursement services. Some are guest-paid or owner-paid. Some are embedded in a property-management system. Some apply only when purchased or activated for a specific reservation.

Damage protection is not a full property policy. It does not replace core property insurance, liability coverage, building coverage, or business-income coverage. Before using a damage-protection product or waiver, understand who pays, product type, covered and excluded damage, claim deadlines, channel differences, and per-stay limits. See provider examples below for Waivo, RentalGuardian, Generali, Safely, and Truvi.

Layer 3: Guest screening and risk prevention

Guest screening reduces the chance of a bad stay. It is not insurance. Screening can include identity verification, fraud checks, payment verification, watchlist screening, reservation risk scoring, or other checks—depending on the provider and jurisdiction.

Follow platform rules, privacy laws, fair housing requirements, consumer protection rules, and applicable local regulations. Digital check-in tools inside a PMS are not a substitute for insurance. See provider examples below for Autohost, Authenticate, Enso Connect, Safely, and Truvi.

Questions to ask before using guest screening

- What exactly is checked? Is the process compliant in my jurisdiction?

- Does it work for direct and OTA bookings? What happens if a guest fails?

- Is consent required? How is personal data stored and deleted?

- Does it integrate with my PMS or booking flow? Is insurance or damage protection included or separate?

Layer 4: Travel insurance and trip protection

Trip protection is usually guest-facing. It helps guests protect their travel investment if they need to cancel or interrupt a trip for a covered reason. For owners, trip protection can reduce cancellation disputes and chargebacks—especially on direct bookings.

Trip protection protects the guest. It does not replace the owner’s property insurance. Do not tell guests they are “fully covered” unless you have read the actual policy language. Offer trip protection through a licensed provider or approved integration rather than informally “selling insurance” yourself. See provider examples below for RentalGuardian, Generali, Allianz, and Arch RoamRight.

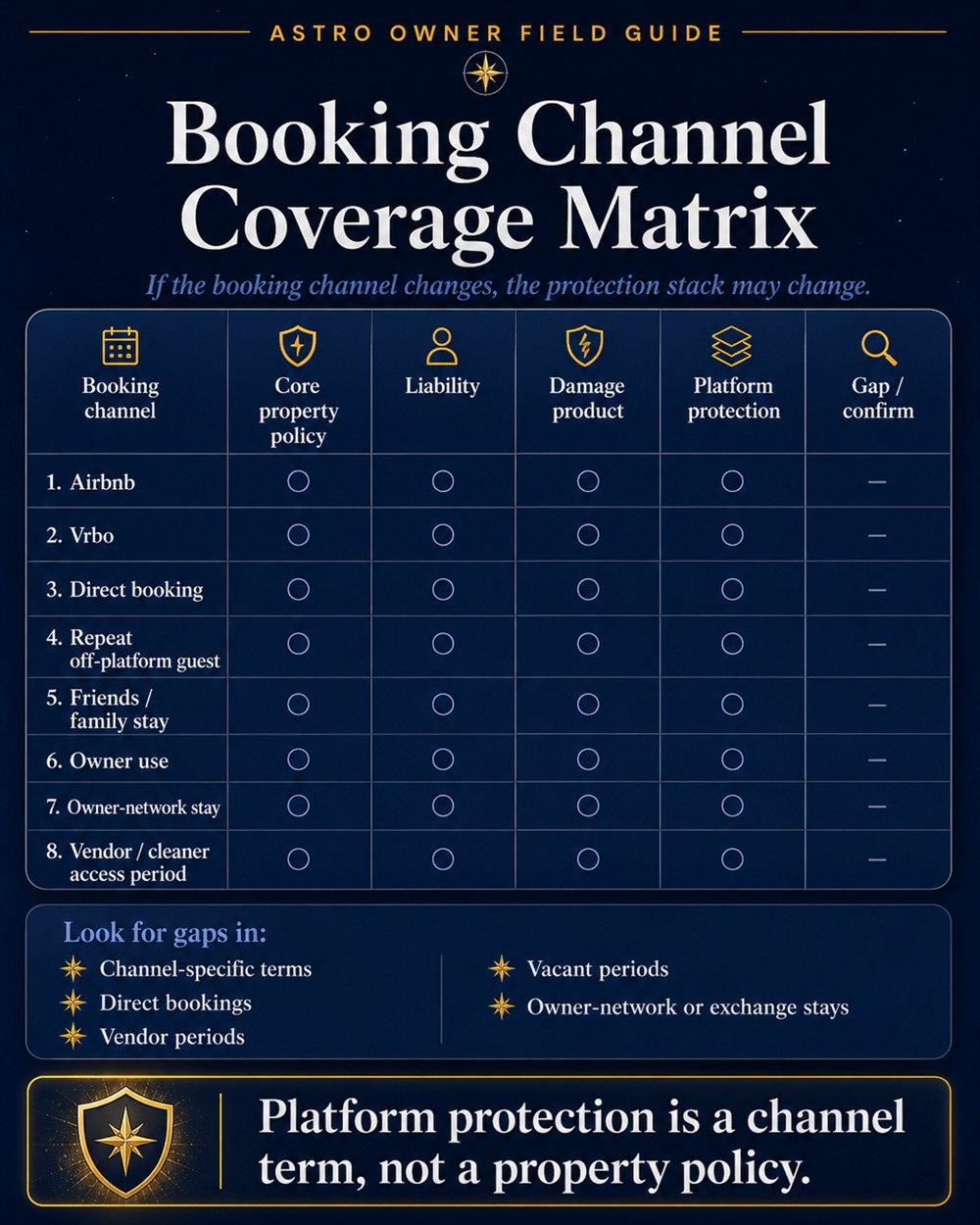

Layer 5: Booking-platform protections — Airbnb, Vrbo, and others

This is the layer many owners misunderstand. Airbnb, Vrbo, and other booking platforms may offer host protections, liability protections, guest-damage processes, optional damage products, claim workflows, or reimbursement tools. These protections can help in certain cases, but they are governed by platform terms.

Platform protections are usually channel-specific. They may not apply to direct bookings, repeat guests who book off-platform, owner-network stays, local rental agreements, blocked calendar periods, vendor activity, or reservations from another channel. For each incident, ask who pays, under what policy, protection product, or platform term, with what exclusions, and what proof is required. See provider examples below for Airbnb AirCover, Vrbo, and other OTAs.

Provider examples: what these companies actually do

The provider names below are examples for owner research, not endorsements.

Do not evaluate a company by its category label alone. Some companies appear in more than one layer because they offer more than one kind of product or service. A company may combine guest screening with damage protection. Another may offer both trip protection and vacation-rental damage protection. Another may be a broker or marketplace rather than the insurance carrier itself.

The important question is not “Have I heard of this company?” The important question is what exactly is being sold, who is protected, which booking channels are included, what limits apply, and what exclusions would matter at your property.

Core STR property insurance examples

Proper Insurance

Proper is a short-term rental insurance specialist. Its public positioning is that its STR policy is a commercial business policy intended to replace inadequate homeowner or landlord coverage for qualifying short-term rental properties, with building, contents, business income, and commercial general liability stated on its materials.

Owners should evaluate Proper when they want a dedicated STR policy that may address building coverage, contents, liability, business income, and vacation-rental-specific risks.

Ask:

- Does this replace my homeowner or landlord policy?

- What building and contents limits apply?

- Is business income or loss of rents covered?

- What liability limit applies?

- Are direct bookings covered?

- Are Airbnb, Vrbo, Booking.com, and repeat guests treated differently?

- Are amenities such as pools, hot tubs, bikes, kayaks, golf carts, docks, fire pits, or grills covered?

- Are bed bugs, theft, pet damage, party damage, or intentional guest damage covered or excluded?

- Is the policy admitted or non-admitted in my state?

- Who is the actual carrier?

Owner translation: Proper is worth comparing if you want an STR-specific policy rather than trying to patch ordinary homeowner coverage.

CBIZ Vacation Rental Insurance

CBIZ Vacation Rental Insurance has insured vacation rental properties since 2002 and positions its product as comprehensive vacation rental insurance for STRs, long-term rentals, dwellings, and vacant properties.

Owners should evaluate CBIZ when they want a vacation-rental-focused policy or brokered insurance path with experience in furnished rental properties.

Ask:

- Is the offered policy specifically built for short-term vacation rentals?

- Who is the carrier?

- What states and property types are eligible?

- Does it cover short-term rentals, long-term rentals, second homes, and vacant periods differently?

- Are guest injury, property damage, owner contents, and loss of income included?

- Are amenities, pets, direct bookings, and mixed owner/guest use covered?

- What optional endorsements are available?

Owner translation: CBIZ may be useful for owners who want vacation-rental-specific insurance guidance, but you still need to read the actual policy form and carrier terms.

Steadily

Steadily markets short-term rental insurance in all 50 states, including damage and liability coverage for Airbnb and Vrbo-style rentals, with rental periods as short as one night on its STR materials.

Owners should evaluate Steadily when they think of the property as an investment property and want a modern quote workflow for rental coverage.

Ask:

- Is this a true STR policy, a landlord policy, or a landlord policy with STR permissions?

- Does it clearly allow nightly or weekly rental use?

- Are direct bookings covered?

- Are furnishings and contents covered?

- Is loss of rents or business income included?

- What happens when the property is vacant between stays?

- Are amenities and pets disclosed and covered?

- What carrier is actually writing the policy?

Owner translation: Steadily may fit some investment-property owners, but do not assume “rental property” automatically means “short-term rental business.”

Obie

Obie is an insurance marketplace focused on landlords and real estate investors. It can help owners compare coverage paths, but the key is the actual policy and carrier behind the quote.

Owners should evaluate Obie when they want comparison shopping or a fast quote workflow.

Ask:

- Is Obie acting as a marketplace, broker, or carrier in this transaction?

- Who is the actual insurer?

- Does the policy explicitly allow short-term rental use?

- Are direct bookings, OTA bookings, owner stays, and vacancy periods covered?

- What endorsements are required?

- What exclusions matter for STRs?

- Are liability, contents, and loss of rents included?

Owner translation: Marketplaces can be useful, but the quote page is not the policy. The policy form controls.

Mainstream carriers and local agents

Mainstream insurers and local agents may offer homeowner endorsements, landlord policies, rental-dwelling policies, or home-sharing options. These can be useful in some cases, especially for occasional rental use or simple properties.

Owners should be careful because “my agent knows I rent” is not the same as “my policy covers repeated short-term rental activity.”

Ask:

- Does the policy explicitly allow repeated STR use?

- Is this occasional home-sharing coverage or full-time vacation-rental coverage?

- Are direct bookings covered?

- Are guest injuries covered?

- Are owner contents and furnishings covered?

- Is business income covered?

- Are amenities, pets, and vendors covered?

- Are there rental-day limits or occupancy restrictions?

- Does the carrier require notice before STR use begins?

Owner translation: Existing-carrier options can work, but only if the policy language matches the actual rental operation.

Damage protection and damage-waiver examples

Waivo

Waivo is a vacation-rental damage protection provider. Its public positioning emphasizes no guest involvement, broad protection, no deductible, and reimbursement workflows for hosts and property managers.

This type of product is not the same as a core property policy. It is a stay-level damage layer.

Ask:

- Is this insurance, a waiver, or a reimbursement service?

- Who is protected: owner, manager, guest, or all of them?

- Does the guest pay a fee? Does the guest need to admit fault?

- What is the per-stay limit? Is there a deductible?

- Does it cover accidental damage only, theft, pet damage, or intentional damage?

- Does it cover contents and building damage?

- Does it apply to direct bookings and OTA bookings?

- What proof is required for reimbursement?

Owner translation: Waivo-type products can reduce security-deposit friction, but they do not replace core property insurance.

RentalGuardian

RentalGuardian provides vacation-rental travel and damage protection products, especially for property managers, software platforms, and booking workflows—with integrated reporting, invoicing, online claims, and manager workflows on its materials.

This type of provider may support both guest-facing travel protection and stay-level damage protection, so owners need to identify which product they are talking about.

Ask:

- Is this trip protection, damage protection, or both?

- Is the product for the guest, the owner, or the property manager?

- Is it integrated into my PMS or booking engine?

- What are the coverage limits? Who files the claim?

- Does it replace a security deposit? What is excluded?

- Are direct bookings included? Does the product require the guest to buy or accept anything?

Owner translation: RentalGuardian belongs in the conversation because it can sit inside the booking flow, but owners must separate guest trip coverage from owner damage protection.

Generali Global Assistance — vacation rental damage protection

Generali appears in two different parts of the STR protection stack: travel insurance and vacation-rental damage protection. That is why generic references to “Generali” are not enough. The relevant product matters. Its damage materials describe accidental damage protection; theft and pet damage may be covered when pets are allowed at the rental, per product terms.

Ask:

- Is this travel insurance or vacation rental damage protection?

- Is the guest buying it? Does it reimburse the guest, the owner, or both?

- Does it cover accidental damage only? Are theft and pet damage included?

- What policy limits apply? What purchase deadline applies?

- What claim documentation is required?

Owner translation: Generali can be relevant for guest-facing trip protection and rental damage protection, but link to the specific product page—not a generic corporate homepage.

Safely

Safely combines guest screening with a protection policy. Its screening materials state screening starts at $5 per screening, or $0.50 per night when combined with the Safely Protection Policy. That is why it appears in both the screening layer and the damage/protection layer.

Ask:

- Am I buying screening only, protection only, or a combined product?

- What does the Safely Protection Policy cover? What liability or damage limits apply?

- Does protection depend on guest screening? What happens if the guest fails screening?

- Does it apply to direct bookings? Does it integrate with my PMS?

- What guest data is collected? What does the guest see? Who files claims?

Owner translation: Safely is prevention plus protection. That can be valuable, but owners should understand both halves.

Truvi

Truvi (formerly Superhog) combines guest screening, verification, damage protection, and claims support for vacation rentals. It is a risk-management product, not just an insurance listing.

Ask:

- Is the product screening, damage protection, claims support, or a bundle?

- Does protection apply only after a guest is screened?

- What is the per-stay damage limit? Are deposits or waivers required?

- Does the tool work across direct bookings and OTA bookings?

- What PMS integrations are supported? What happens if a guest is flagged?

- What documentation is required for a claim?

Owner translation: Truvi appears in multiple layers because the product combines prevention and protection. That should be explained, not hidden.

Guest-screening and verification examples

Autohost

Autohost is a guest-screening and verification platform for short-term rental and hospitality operators. It focuses on screening, fraud prevention, risk scoring, and chargeback reduction. It is not a property insurance policy.

Ask:

- What checks are performed? Does it verify ID?

- Does it screen for fraud or chargeback risk? Does it perform background checks?

- Does it comply with applicable law in my jurisdiction?

- What happens if a guest is flagged? Does the guest need a separate flow?

- Does it integrate with my PMS? Is any damage protection included, or screening only?

Owner translation: Autohost is a prevention layer. It may help avoid bad stays, but it does not pay property claims by itself.

Authenticate

Authenticate offers guest-verification and background-check-oriented tools. This can be useful for owners who need stronger verification for direct bookings or higher-risk stays.

Ask:

- What databases or checks are used? Is guest consent collected?

- Are consumer-reporting rules implicated? Is the process legal in my state and for my use case?

- What does the owner receive after screening? What does the guest see? How are records stored?

Owner translation: Background checks can create legal obligations. Do not use them casually.

Enso Connect

Enso Connect is primarily a guest-experience and digital guest journey platform. It may support guest verification, check-in flows, upsells, guidebooks, and messaging. It should not be described as an insurance provider.

Ask:

- Is the relevant feature guest verification, check-in, messaging, upsells, or guidebook functionality?

- Does it verify ID? Does it collect signatures or agreements?

- Does it integrate with locks or guest access? Does it include insurance or only workflow support?

- Does it comply with platform rules?

Owner translation: Enso Connect is more guest-flow infrastructure than insurance. It may support a risk process, but it does not replace coverage.

Travel insurance and trip-protection examples

RentalGuardian / Travel Guardian

RentalGuardian also belongs in the trip-protection layer because it supports travel protection products in vacation-rental booking flows.

Ask:

- Is the plan available to this guest? Is it offered at checkout?

- What cancellation or interruption reasons are covered?

- Does it include weather, illness, injury, delay, or evacuation benefits?

- What is the maximum trip cost and trip length?

- Does it affect my cancellation policy? Who services the claim?

Owner translation: Guest trip protection can reduce cancellation friction, but it protects the guest’s trip investment, not the building.

Generali Global Assistance — travel insurance

Generali’s travel insurance products may cover trip cancellation, interruption, travel delay, medical events, evacuation, or vacation-rental-related losses depending on the plan. Confirm which plan is offered.

Ask:

- Which plan is being offered? Is the guest eligible?

- Does it cover vacation rental costs?

- What are the covered cancellation reasons? Are named storms or evacuations covered?

- Are pre-existing condition rules relevant? What documentation does the guest need?

Owner translation: Travel insurance should be explained as guest-facing protection. It does not insure the owner’s property.

Allianz Travel Insurance

Allianz offers travel insurance plans. At least some Allianz plans reference vacation rental costs as prepaid, non-refundable expenses that may be reimbursable if cancellation is for a covered reason.

Ask:

- Which Allianz plan is being offered? Does it cover vacation rental lodging costs?

- What reasons are covered for cancellation?

- What trip interruption, delay, medical, or baggage benefits apply?

- Is there a review period? Does coverage vary by state?

- Is this offered through a licensed integration or purchased directly by the guest?

Owner translation: Allianz is a recognizable trip-protection option, but it is still guest-facing travel insurance.

Arch RoamRight

Arch RoamRight offers travel insurance products. Link to the specific current plan or provider page when comparing—not a stale or generic reference.

Ask:

- Which plan is current? What benefits apply to vacation rental travelers?

- What cancellation and interruption reasons are covered?

- Does coverage vary by state or traveler residence?

- What are the claim deadlines and documentation rules?

Owner translation: Keep Arch RoamRight only if you can link to a current, relevant product page.

Booking-platform protections

Airbnb AirCover for Hosts

Airbnb AirCover for Hosts includes host damage protection and host liability insurance components, but it is governed by Airbnb’s terms.

Ask:

- Does it apply to this reservation? What deadlines apply? What is excluded?

- What proof is required? Does it apply outside Airbnb?

- How does it interact with my own insurance? Is this damage protection, liability insurance, or both?

Owner translation: AirCover can help on eligible Airbnb bookings. It is not your property policy.

Vrbo protections

Vrbo may provide liability protection for eligible reservations and may offer or facilitate accidental damage protection options. The exact protection depends on the reservation, terms, and any product purchased.

Ask:

- Does the liability protection apply to this reservation? Did the guest purchase accidental damage protection?

- What limit applies? What deadline applies? Who files the claim?

- Does it apply outside Vrbo? What is excluded?

Owner translation: Vrbo-related protection is booking-channel protection. It does not travel automatically to direct bookings or other platforms.

Other OTAs

Other booking channels may have deposits, damage workflows, claim tools, or liability language, but every platform is different.

Ask:

- Is this an actual insurance product or just a platform process?

- Is the booking eligible? What proof and deadlines apply?

- What happens if the guest denies responsibility?

- Does the process cover direct bookings or only platform bookings?

Owner translation: Never assume one platform’s protection rules apply to another platform.

How owners should compare providers

Do not compare providers by headline marketing copy alone. Use a practical comparison framework.

1. Coverage or protection type

Is it a property insurance policy, liability policy, homeowner endorsement, landlord policy, damage-protection product, damage waiver, guest-screening service, identity-verification tool, travel insurance plan, trip-protection product, platform claim process, service contract, or reimbursement process? These are not interchangeable.

2. Booking channels

Confirm whether protection applies to Airbnb, Vrbo, Booking.com or Expedia, direct bookings, repeat guests, owner-network stays, friends and family stays, mid-term stays, owner use, blocked calendar periods, and unoccupied periods.

3. Covered risks

Ask whether the policy, product, service, or platform term addresses guest and visitor injury, vendor injury, fire, water damage, theft, vandalism, guest-caused damage, pet damage, contents, loss of income, amenity-related incidents, weather, sewer backup, pests, party damage, intentional acts, and criminal activity.

4. Limits, deductibles, and exclusions

Know coverage limits, sublimits, deductibles, exclusions, claim deadlines, required documentation, replacement cost vs actual cash value, business income coverage, amenity disclosure, and whether undisclosed use can void coverage.

5. Claims process

Before a claim happens, know who files, where to file, filing deadlines, required photos and reports, preserved guest communication, invoices and estimates, whether the booking platform must be contacted first, deductibles, and whether a guest can be charged directly.

Ask for the numbers

Premiums and limits vary widely by state, replacement cost, amenities, occupancy, and claims history. This guide does not quote the market—but you should ask for concrete figures when comparing policies or protection products:

- liability limit;

- property coverage limit;

- contents / furnishings limit;

- business income or loss-of-rents limit;

- deductible;

- per-stay damage protection limit;

- trip protection limits;

- claim filing deadline;

- guest damage documentation deadline;

- exclusions and sublimits for pools, hot tubs, docks, pets, events, or amenities.

What the warnings actually mean

Insurance language can sound abstract until a claim happens. These are common warnings owners see in insurance guides, translated into practical terms.

“Confirm short-term rental use in writing”

This means your policy should clearly allow the way you actually rent. A homeowner policy might tolerate a one-time guest rental but exclude repeated business use. A landlord policy might cover a long-term tenant but not nightly guests.

Owner example: if a guest slips near the hot tub and your carrier decides the home was being used as an undisclosed business, the problem is whether the policy covered this use—not whether you had insurance at all.

“Ask who the actual carrier is”

Some companies are carriers; some are brokers, marketplaces, or agencies. The company whose website you used may not be the company that pays or denies the claim. Ask who is the insurer, who is the broker, who administers claims, whether the policy is admitted or non-admitted in your state, and where to find the actual policy form.

“Admitted versus non-admitted”

An admitted carrier is licensed by the state and participates in that state’s insurance regulatory system. A non-admitted or surplus-lines carrier may still be legitimate but is regulated differently and may not have the same state guaranty protections if the insurer fails. Ask your agent what admitted or surplus-lines coverage means in your state.

“Replacement cost versus actual cash value”

Replacement cost may pay based on what it costs to replace a damaged item with a new comparable item, subject to policy terms. Actual cash value usually subtracts depreciation. If the property is full of furniture and electronics, valuation method matters. Ask whether contents are covered at replacement cost or actual cash value and whether sublimits apply.

“Sublimits”

A sublimit is a smaller limit inside the larger policy limit. You might have a large property limit but a much smaller limit for theft, water backup, outdoor property, or guest-caused damage. Ask what sublimits apply to STR-relevant losses and amenities.

“Business income” or “loss of rents”

This usually means coverage for rental income lost after a covered property claim—not an empty calendar or demand drop. Ask whether loss of rents is included, what triggers it, how income is calculated, whether there is a waiting period, and whether direct and OTA bookings are both counted.

“Amenity exclusions”

Pools, hot tubs, docks, kayaks, golf carts, fireplaces, and waterfront access can all affect coverage. Ask whether all amenities are disclosed, excluded, or subject to rules, signs, or waivers.

“Direct bookings may be different”

A platform booking may come with platform protections; a direct booking usually does not. Ask whether your property policy and damage protection apply to direct bookings, whether you need a rental agreement, guest screening, or licensed trip protection.

“Guest-facing protection is not owner protection”

Trip insurance usually protects the guest’s trip investment. It does not usually protect the owner’s building, furnishings, or liability. Ask who is insured, who receives payment, and what is protected.

“Waiver versus insurance”

A damage waiver is not always the same as insurance. A waiver may limit guest pursuit for certain accidental damage; insurance involves an insurer, policy forms, and regulated claims handling. Ask product type, who backs it, limits, and whether the guest remains responsible above the limit.

“Claim deadlines”

Many protections require quick action—platform notice before the next guest, damage product photos within a set period, prompt notice to the carrier. If you discover damage after additional turnovers without photos or cleaner notes, the claim becomes harder.

“Documentation requirements”

Coverage is only useful if you can prove the loss. Maintain pre-stay photos, post-stay damage photos, cleaner reports, guest messages, repair invoices, inventory lists, maintenance logs, and platform claim records.

“Platform protection is channel-specific”

Airbnb protection is for eligible Airbnb bookings; Vrbo protection is for eligible Vrbo bookings. They do not automatically apply to direct bookings, repeat guests, or other channels. Ask which channel was used and what your independent policy covers regardless of channel.

“Do not assume your PMS integration equals coverage”

A PMS integration can make it easier to offer screening or damage protection, but integration is not coverage. Ask whether the product is turned on, which properties and channels it applies to, and whether guest acceptance is required.

A practical owner protection stack

- Core STR property insurance — the foundation.

- Damage protection — stay-level guest damage protection, especially for direct bookings.

- Guest screening — a prevention layer.

- Trip protection — guest-facing booking protection.

- Booking-platform protection — channel-specific protection, not complete coverage.

Each layer serves a different purpose. Remove one layer and overall protection may become weaker.

Owner action plan: what to do this week

1. Pull your current policy documents

Gather declarations pages, full policy forms, endorsements, exclusions, umbrella policy (if any), and HOA, condo, or mortgage insurance requirements as relevant.

2. Ask your agent or carrier in writing

Ask whether the policy covers repeated short-term rental use, including direct bookings and OTA bookings. Also ask about guest injuries, guest-caused damage, furnishings, business income, amenities, vendors, pets, events or parties, channel differences, and claim documentation.

3. Map your booking channels

List every place guests can book, then identify which policy, protection product, service, or platform term applies to each channel.

4. Document your property condition

Create a repeatable process: pre-season photos, furnishing inventory, appliance serial numbers, receipts for major purchases, maintenance and amenity inspection logs, cleaning reports, check-in and check-out records, incident reports, and preserved guest communications.

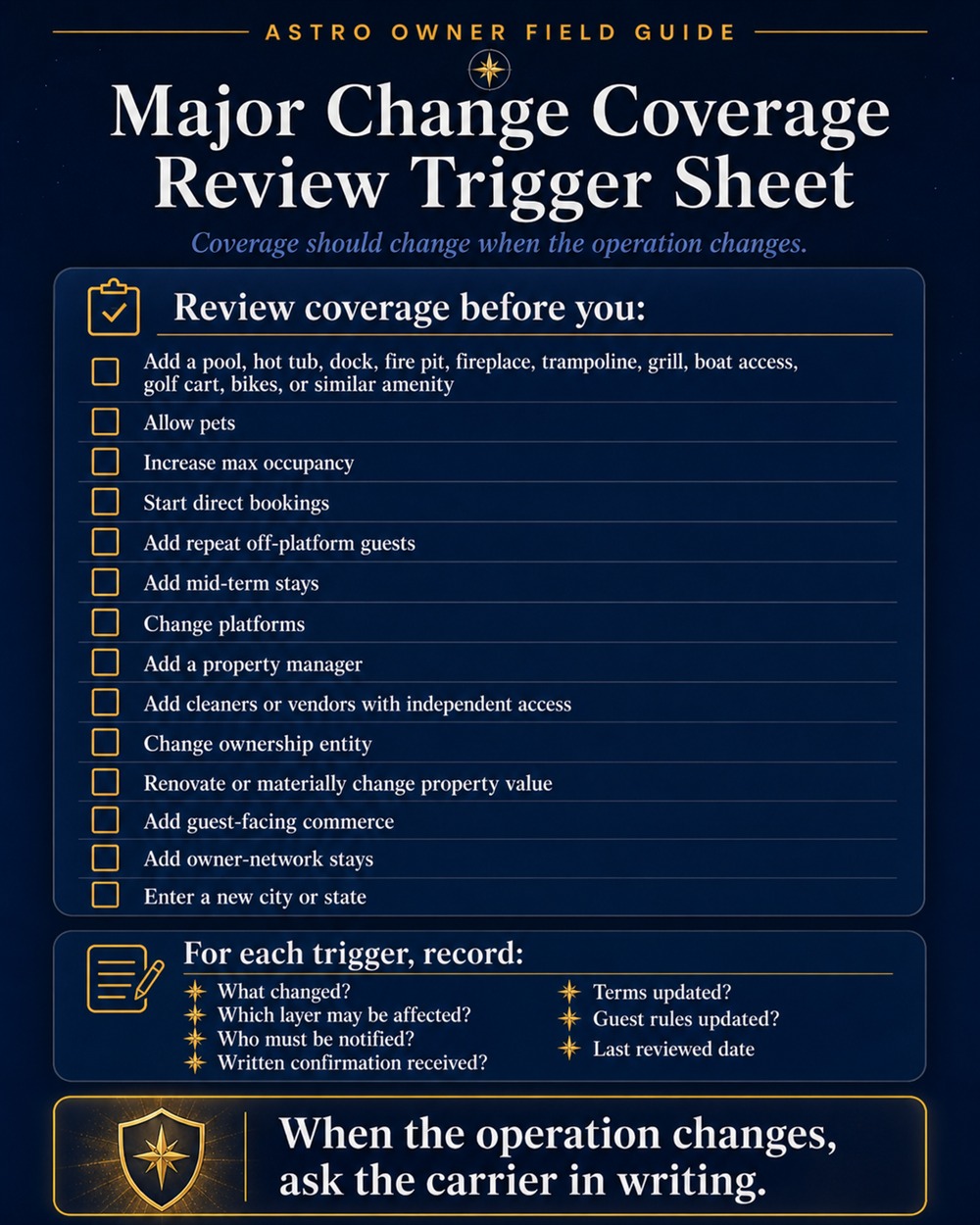

5. Review your risk after any major change

Recheck coverage when you add amenities, allow pets, increase occupancy, start direct bookings, add mid-term stays, change ownership structure, add a property manager, renovate, enter a new market, change platforms, activate owner-network or exchange participation, or add property-level guest services or commerce.

Why this matters for ASTRO owners

ASTRO is built for short-term rental owners, not casual travel shoppers.

That means property identity, owner verification, guest-facing operations, direct booking posture, owner-network stays, and property programs all need clean boundaries. Insurance belongs in that same operating discipline.

ASTRO does not sell insurance, does not replace property insurance, and does not verify insurance on behalf of owners in this release. But an owner who understands their protection stack is better prepared to operate inside a serious owner network.

This matters because ASTRO owners may eventually manage more than one kind of property activity:

- ordinary OTA bookings;

- direct bookings;

- guest-facing property tools;

- owner-network stays;

- property-level programs such as Guest Portal, AArtners, Honor Pantry, Home Showcase, Concierge, or City Watch;

- vendor, artist, service, or partner relationships connected to a property.

Those activities are not all covered the same way.

A registry identity is not an insurance policy. Listing-control verification is not liability coverage. Owners Exchange settlement mechanics do not insure the building. Guest Portal content does not replace a property policy. ASTRO programs can add owner value, but they do not replace core STR insurance, damage protection, guest screening, trip protection, or booking-platform terms.

That is the practical reason this guide belongs here: ASTRO is helping owners think clearly about the operating layers around a short-term rental property.

Before you add channels, programs, amenities, direct bookings, owner-network stays, or guest-facing tools, know what protects the property underneath them. When you are ready to align property identity and verification with how you operate, explore the registry or join ASTRO.

Common mistakes owners make

- Assuming a homeowner or landlord policy covers nightly rentals without written confirmation.

- Treating platform host protection as a substitute for a property policy on direct bookings.

- Adding amenities, pets, or higher occupancy without updating the carrier or disclosure records.

- Mixing up damage waivers, reimbursement services, and actual insurance products.

- Missing claim deadlines or failing to document pre-stay condition before a loss.

- Calling third-party insurance or OTA protections “ASTRO programs” when they are separate operating layers.

The Simplest Counterargument

Many owners do not need a complicated protection stack. Most will never face a catastrophic claim. Additional policies, endorsements, waivers, documentation procedures, and operational processes add cost and administrative burden. An owner may spend years paying for overlapping protections that never provide meaningful value.

That objection is reasonable. Complexity has a real price—in premiums, products, staff time, and attention.

What Still Matters

Not every owner needs the same stack. Not every owner needs more insurance. Not every owner needs additional products.

But every owner should know what risks they are actually exposed to and what protections they are actually relying on.

The goal is not to buy every available policy or protection product. The goal is to make sure the protection you think you have is the protection you actually have.

Make sure your insurance covers what you want it to cover.

Understand what your booking platform does and does not protect. Understand what your policy does and does not cover. Understand where the gaps are. Then make an informed decision about whether those gaps matter for your property, your guests, and your risk tolerance.