Deposits, Waivers, and the Money Between Prevention and Insurance

What owners need to understand before something goes wrong

You've built a safe and durable property so that most incidents never happen. You understand the insurance protection stack that backstops the rare, serious loss. This guide is about the layer in between — the everyday money tools that handle the minor, guest-caused damage that prevention couldn't stop and that's far too small to ever touch a property policy.

These are the non-insurance protections: security deposits, damage waivers, and third-party damage-protection products. They share a job — recovering the cost of ordinary guest-caused damage — but they work in completely different ways, carry different risks, and are governed by different rules. Owners routinely confuse them, and the confusion is expensive.

Here's the order of operations again, this time with the middle filled in:

- Prevention — a safe, durable, well-maintained property. See The Safe and Durable Property.

- Non-insurance protections — deposits, waivers, and damage-protection products for first-dollar, guest-caused damage. This guide.

- Insurance and the protection stack — the backstop for the rare, serious, or catastrophic loss. See the 5-layer protection stack.

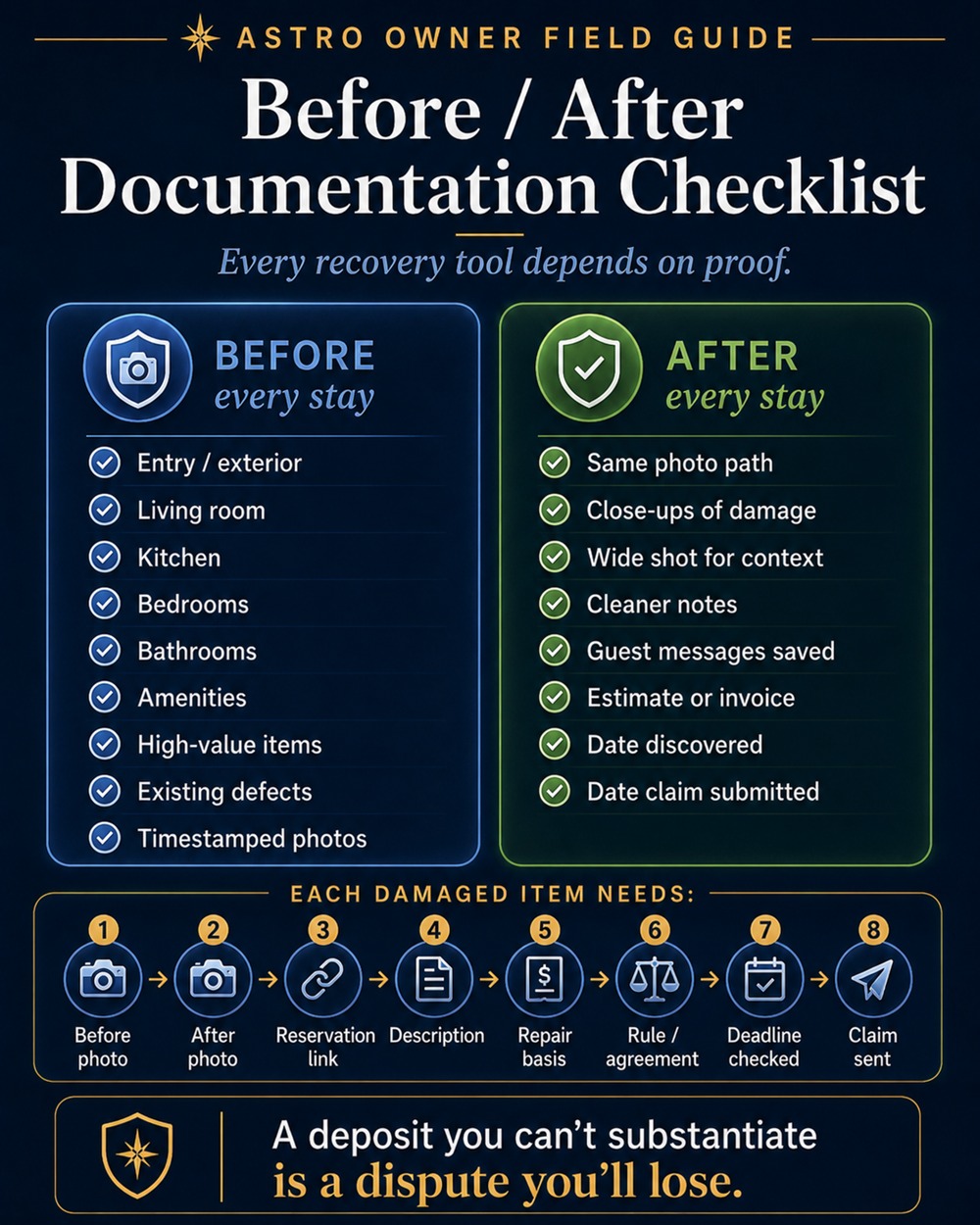

Two things to hold in mind throughout. First, none of these tools is insurance on your building, your liability, or your lost income — they recover specific, attributable, guest-caused damage and nothing more. Second, every one of them only works if you've done the documentation. A deposit you can't substantiate is a dispute you'll lose; a waiver you can't claim against is a fee the guest paid for nothing.

Tension: collecting money is the easy part

Common bad assumption:

"I take a deposit, so I'm covered for damage."

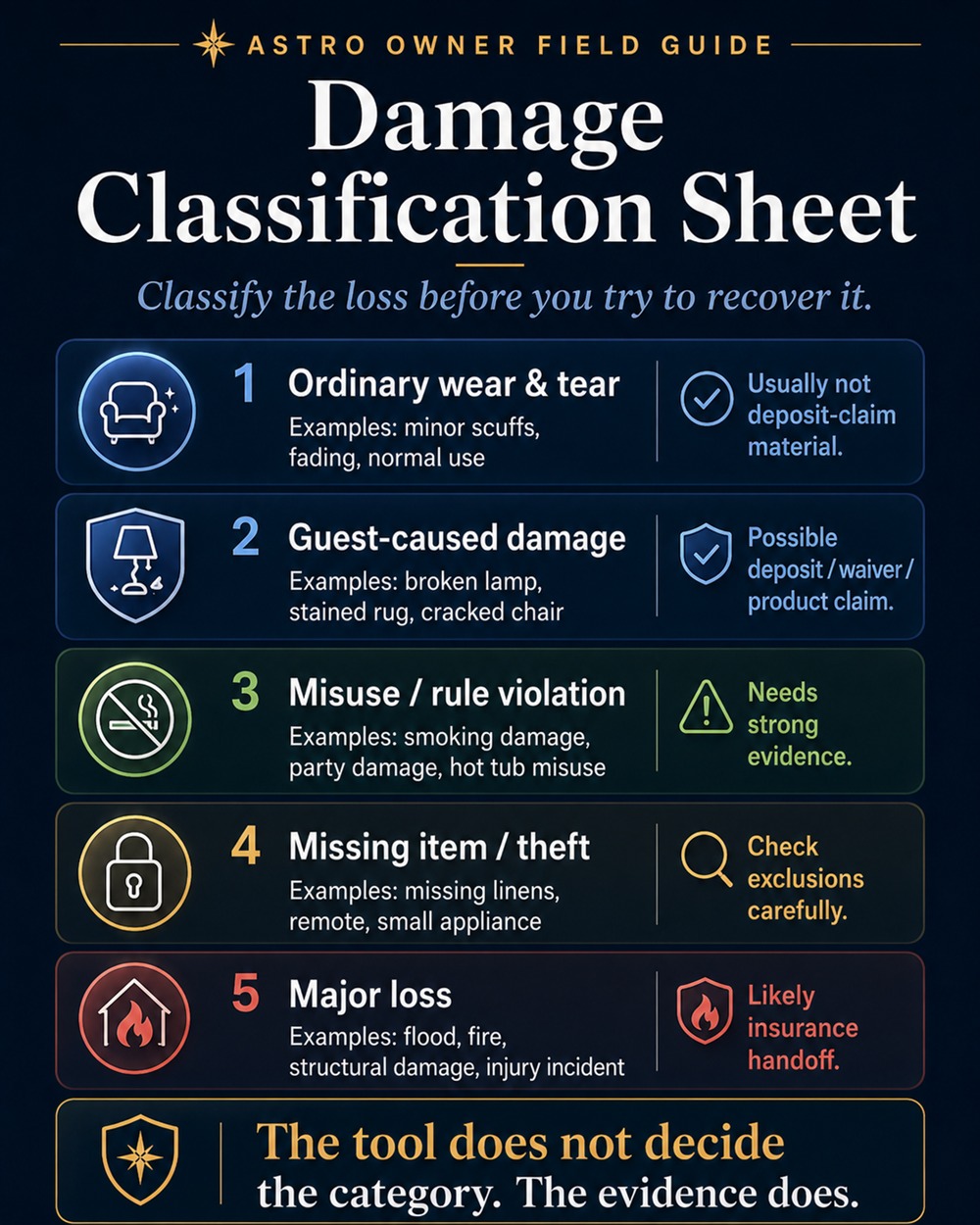

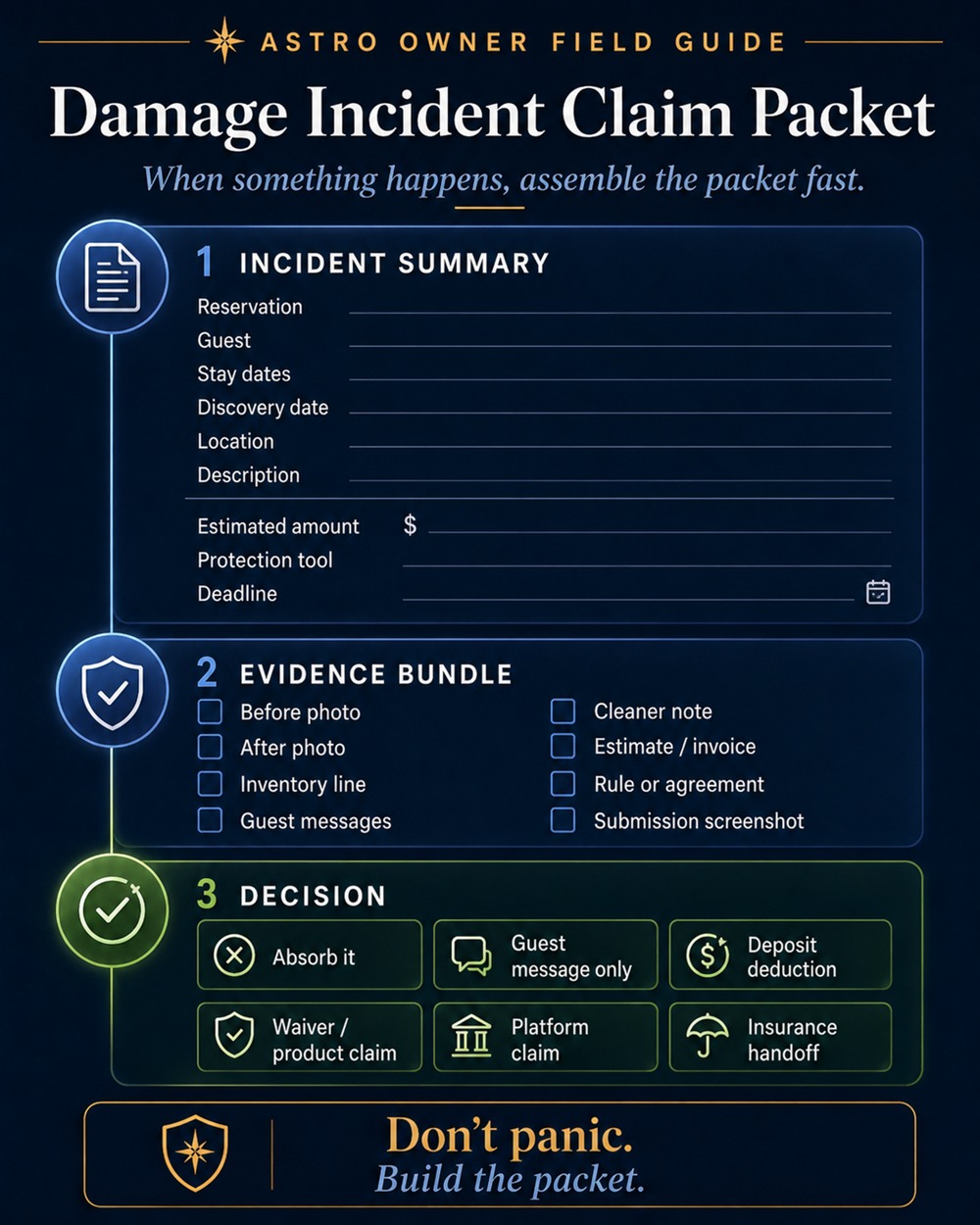

Holding a deposit and successfully recovering against it are two very different things. To actually keep deposit funds for a damaged item, you generally need to show the damage occurred during the guest's stay, that it exceeds ordinary wear and tear, what it costs to repair or replace, and that you followed the platform's process and your jurisdiction's rules — within the deadlines. Miss any of those and the money goes back, often with a strike against your account.

That's the core tension. The friction in deposits and waivers isn't collecting the money. It's the burden of proof, the platform rules, the local regulations, the deadlines, and the guest relationship you may not want to torch over a stained towel. Choosing the right tool is mostly about choosing where you want that friction to live.

The tools, and what each one actually does

Security deposits

A security deposit is money associated with a reservation that you can claim against if the guest causes damage, and that otherwise returns to the guest. In practice it shows up in a few forms:

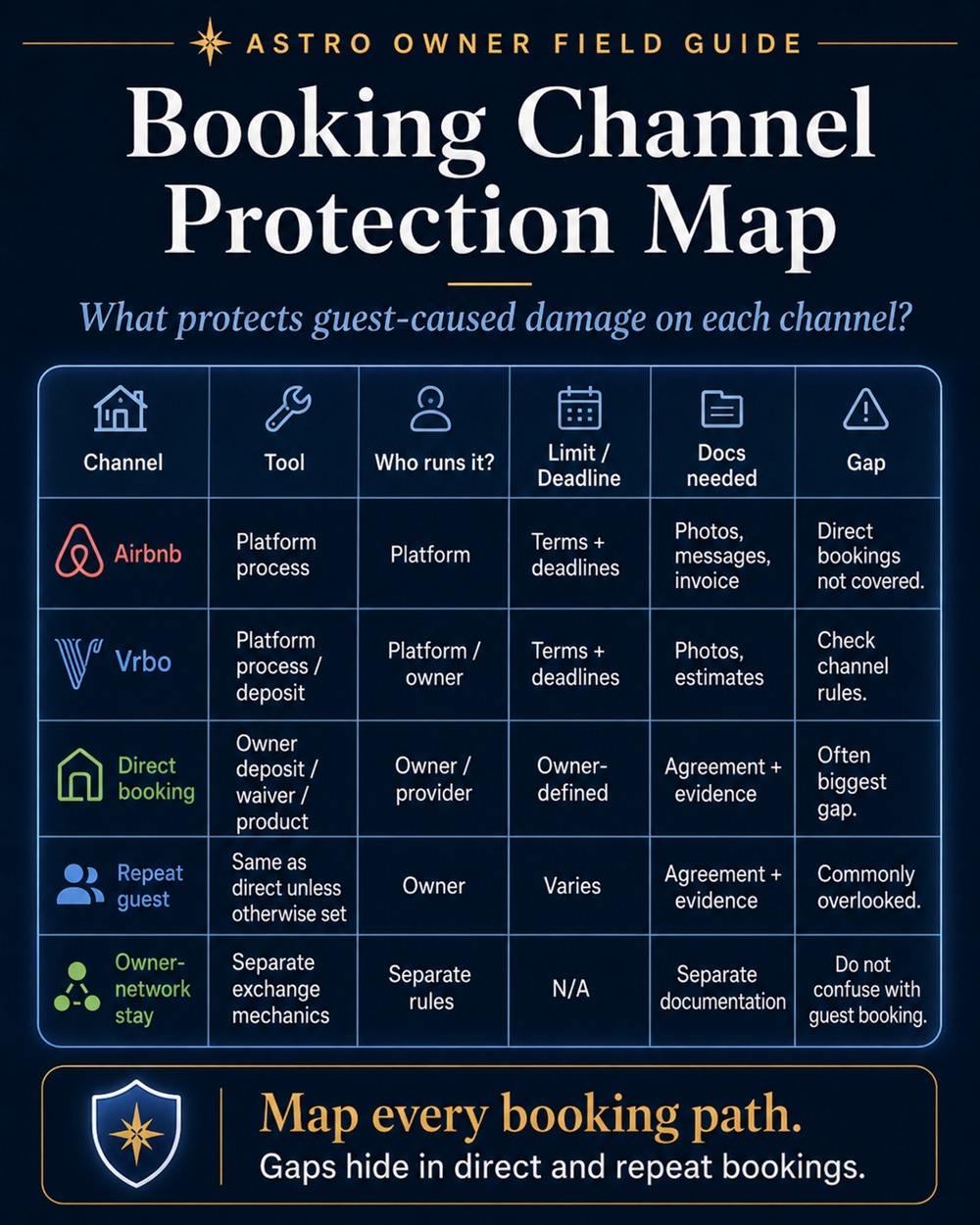

- A true hold or pre-authorization — funds are reserved on the guest's card and released if unused. Common, low-friction for honest guests, but the held amount is usually modest relative to real damage potential.

- A platform-administered deposit — collected and adjudicated under the booking platform's rules, on the platform's timeline, with the platform as referee. You play by their process.

- An owner-collected deposit — you hold the funds directly, typically on direct bookings. More control, but also more responsibility: you're now subject to the local rules on how deposits must be held, accounted for, and returned, and you carry the dispute risk yourself.

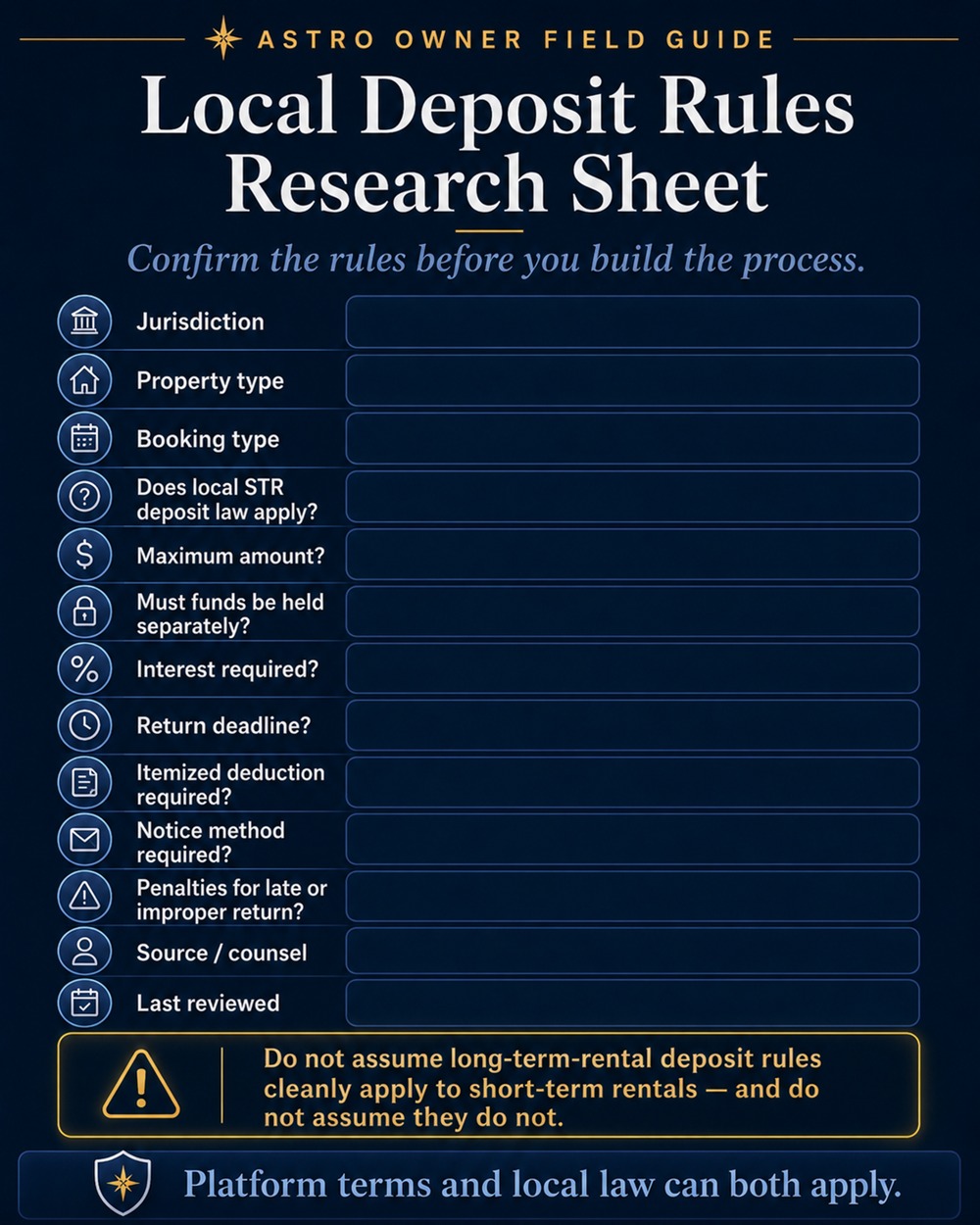

What owners get wrong about deposits: they assume the deposit sets the ceiling on what they can recover (it usually doesn't — it's just the easy-to-reach money), and they underestimate how regulated and time-bound the return process can be. Deposit handling for short-term rentals is governed by a patchwork of platform terms and local law that varies widely by jurisdiction; this is precisely the kind of thing to confirm rather than assume.

Damage waivers

A damage waiver flips the model. Instead of holding refundable money, the guest pays a typically non-refundable fee, and in exchange accidental damage up to a stated limit is covered without a hold to argue over later. The guest experience is smoother — no large authorization on their card, no post-stay tug-of-war — and the friction shifts from the back end (chasing a deposit) to the front end (a small added cost on every booking).

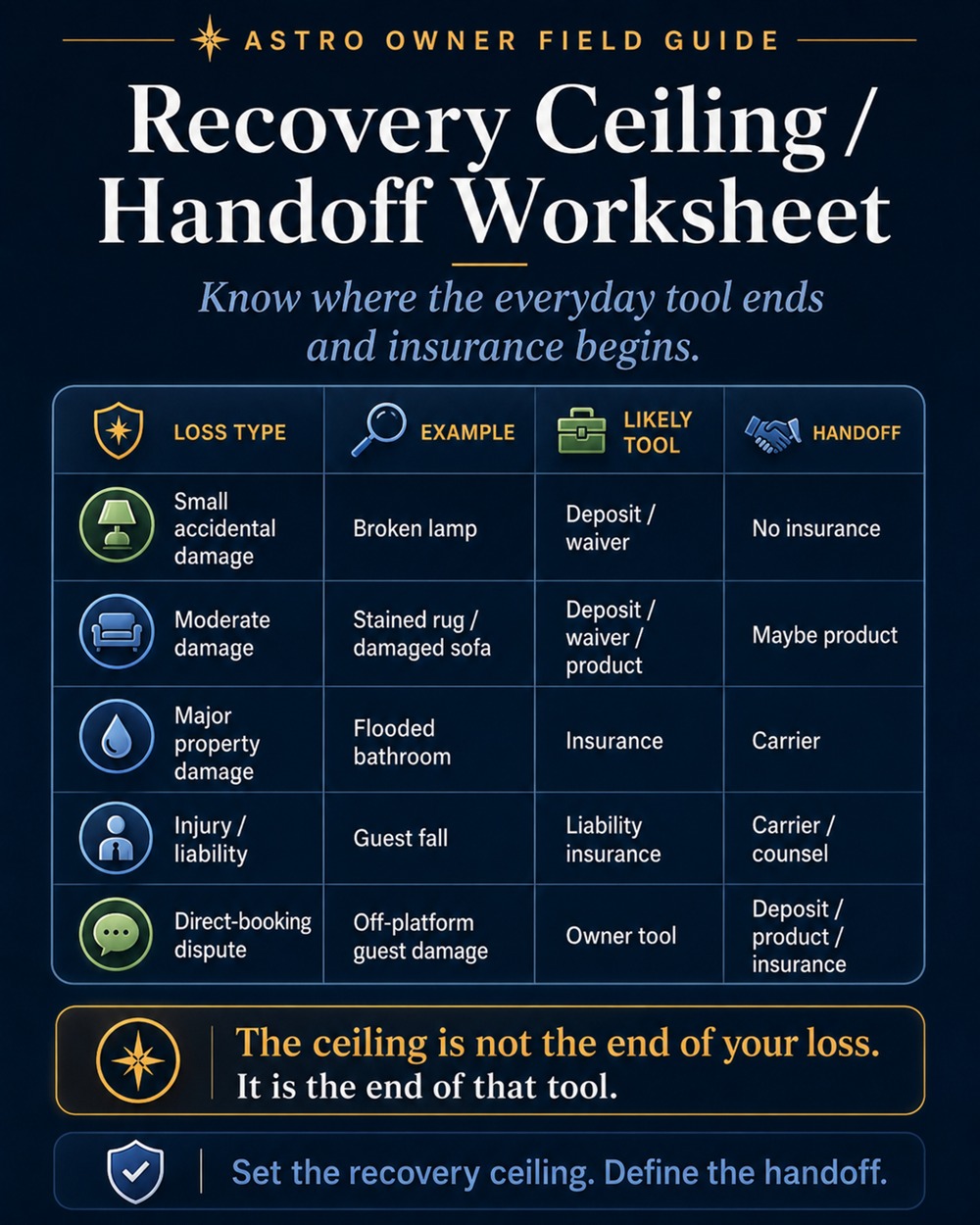

Waivers suit high-turnover properties, direct bookings, and owners who'd rather price a little protection into every stay than fight occasional deposit disputes. The watch-outs: know the coverage limit, what counts as accidental versus excluded (intentional damage, theft, and gross misuse are commonly excluded), who administers the claim, and the deadlines. A waiver that covers $1,500 of accidental damage does nothing for the $4,000 incident — that's where your deposit ceiling, and ultimately your policy, come back into play.

Third-party damage-protection products

A growing set of providers sell stay-level damage protection that bolts onto your booking flow or property-management system. This is where naming discipline matters, because these are not all the same legal thing — and the insurance protection stack guide treats this category as Layer 2 of the stack for exactly this reason:

- Some are insurance products (an insurer pays a covered claim).

- Some are damage waivers (a contractual fee-for-coverage arrangement).

- Some are reimbursement services (a process that pays out under its own terms).

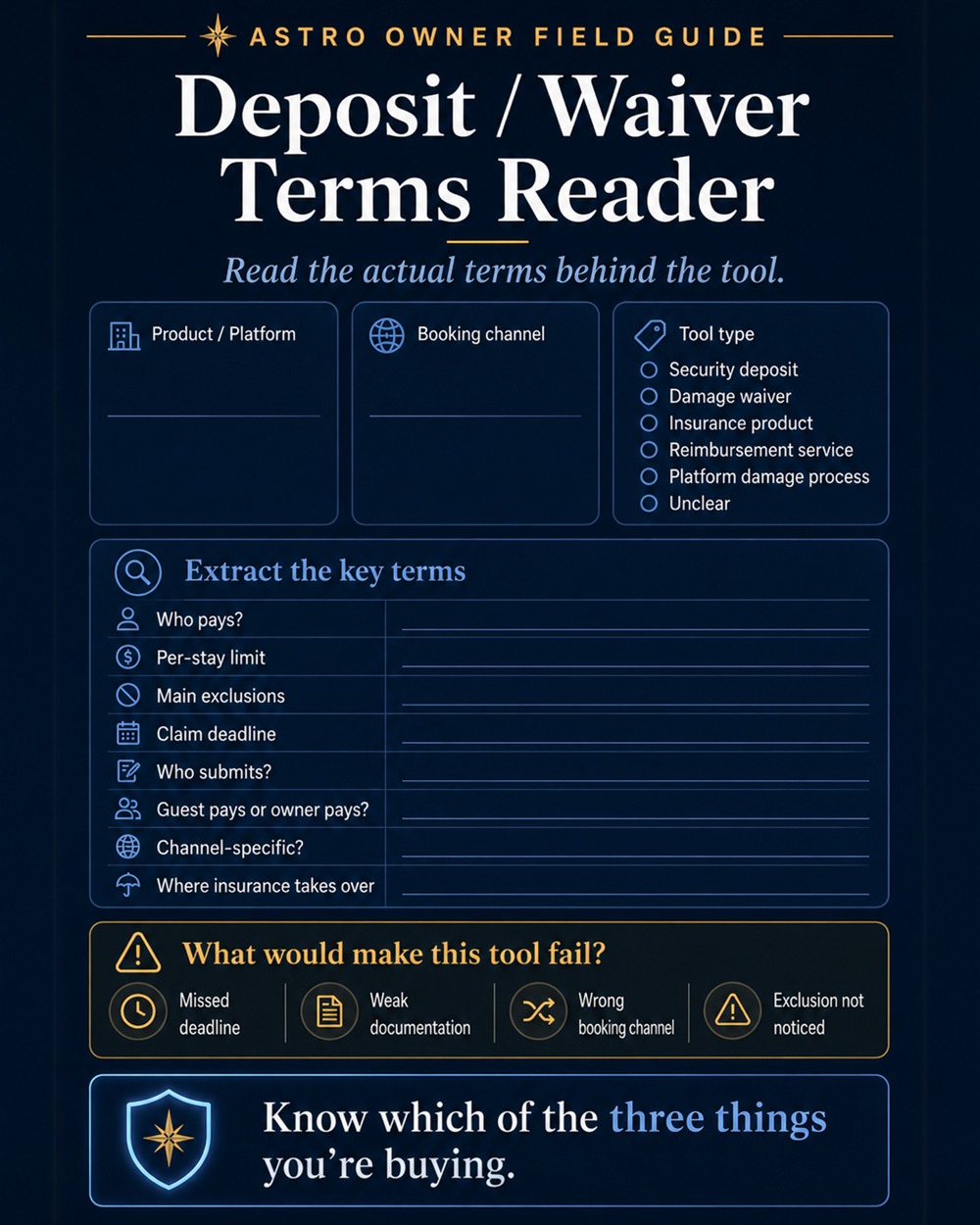

Before relying on any of them, pin down who pays, the product type, what's covered and excluded, claim deadlines, whether it differs by booking channel, whether the guest or you pays, and the per-stay limit. The providers compared in the insurance guide's Layer 2 are the place to start your research; this guide's point is simply that you should know which of the three things you're buying.

Booking-platform damage processes

Airbnb, Vrbo, and other channels run their own guest-damage and reimbursement processes — channel-specific, deadline-driven, and governed by their terms. These blur the line between "non-insurance protection" and "platform protection," and the protection stack guide covers them in depth as Layer 5. The single thing to carry over here: a platform damage process generally applies only to bookings made on that platform. Your direct bookings, repeat off-platform guests, and owner-network stays need their own deposit or waiver arrangement, because the platform's process won't reach them.

The two things that make any of these work

None of the tools above functions in a vacuum. Two unglamorous pieces sit underneath all of them:

- A written rental agreement and clear house rules — the contractual backbone that defines what the guest is responsible for, what counts as damage versus wear, and what the deposit or waiver covers. Without it, recovery is an argument; with it, recovery is enforcement.

- Documentation — date-stamped condition photos before and after, a furnishing inventory, receipts, repair estimates, and preserved guest communication. This is the same evidence trail the insurance layer depends on; the protection stack guide lays out the full process, and it does double duty here. Guest screening — covered as Layer 3 of that guide — belongs to the prevention side of this equation: the best deposit dispute is the one a well-screened guest never causes.

How owners should choose: deposit vs. waiver vs. product

There's no universal right answer; there's a right answer for your property, channel mix, and tolerance for friction. A practical way to decide:

1. Where do you want the friction?

A deposit puts the friction at the back end — after a problem, when you're proving and claiming. A waiver puts it at the front end — a small, predictable cost on every booking, in exchange for fewer post-stay fights. Owners who hate disputes often prefer waivers; owners with low damage rates and disciplined documentation often prefer deposits.

2. What's your booking channel mix?

Platform-administered deposits and platform damage processes only cover that platform. The more you rely on direct bookings and repeat guests, the more you need a deposit or waiver arrangement you control end to end.

3. What's the realistic loss size?

Match the tool to the exposure. Modest holds and waivers handle the broken lamp and the stained rug. They are not built for the flooded bathroom or the party that wrecks a room — that's where your deposit ceiling is exceeded and the insurance protection stack takes over.

4. What does your jurisdiction allow?

Some places regulate short-term rental deposits — how much, how held, how and when returned. Confirm what's permitted before you build a process around it. Platform terms and local law both apply, and they don't always agree.

5. What can you actually document and enforce?

The most sophisticated protection is worthless if you can't substantiate a claim. If your operation can't reliably produce before/after photos, an inventory, and a written agreement, fix that first — it determines whether any of these tools will hold up.

Owner action plan: what to do this week

1. Inventory your current setup

For each way guests can book you, write down exactly which protection applies: a hold, a platform deposit, a waiver, a third-party product, or nothing. Gaps usually hide in direct bookings and repeat guests.

2. Read the actual terms

Pull the real terms behind your damage waiver or protection product and classify it: insurance, waiver, or reimbursement. Note the limit, exclusions, claim deadline, and who pays.

3. Put a rental agreement and house rules in writing

If you don't have a clear, current agreement that defines guest responsibility and what the deposit or waiver covers, that's the highest-return thing you can fix this week. It's the difference between enforcing a claim and arguing one.

4. Build the documentation habit

Standardize date-stamped before/after photos, a furnishing inventory, and preserved guest messages for every stay. This is the same evidence the insurance layer needs, so you're building it once for both.

5. Confirm the local rules

Check your jurisdiction's rules on short-term rental deposits — amount, holding, and return timelines — before relying on a deposit-based process.

6. Connect the layers

Decide your tool per channel, set a realistic recovery ceiling, and know exactly where the handoff to insurance begins. Prevention shrinks how often you reach for any of this; see The Safe and Durable Property.

Where this shows up in ASTRO

ASTRO is built for short-term rental owners, but ASTRO does not hold, collect, administer, or adjudicate guest deposits; does not sell, provide, or endorse damage waivers or damage-protection products; and does not act as referee in any guest-damage dispute in this release. Deposits, waivers, and protection products are arrangements between owners, their guests, their chosen providers, and their booking platforms.

ASTRO's role is to help owners operate with clearer identity, registry, trust, and owner-program boundaries — and to share practical owner education like this guide.

- Explore properties — registry identity and trust posture.

- Join ASTRO — membership and property claim workflows.

- Owners Exchange — owner-to-owner stays are governed by exchange mechanics; they are not the same as a guest reservation, and they do not use guest deposits or waivers. Exchange mechanics are separate from the tools in this guide.

A deposit, waiver, or protection product is an owner operating choice. It is not an ASTRO program, and naming a third-party product an "ASTRO program" mixes up layers that should stay separate — the same distinction the insurance guide draws.

Operator Reality

Pick one booking channel you use most. Write down, in one line, exactly what protects a guest-caused-damage incident on that channel today — and whether you could actually prove and claim it. If the honest answer is "I'm not sure," you've found your week's work: a written agreement, a documentation habit, and a clear decision between deposit and waiver. Then map the same line to your direct bookings, where the protection is most often missing.

Common mistakes owners make

- Treating a deposit as proof of coverage rather than a recovery tool that has to be substantiated and enforced.

- Confusing a damage waiver, a reimbursement service, and an actual insurance product — they are three different things.

- Assuming a platform's damage process covers direct or repeat off-platform bookings.

- Setting a deposit or waiver limit that has no relationship to the property's real loss potential.

- Skipping the written rental agreement, then trying to enforce terms that were never agreed to.

- Failing to document pre-stay condition, then losing the dispute on proof.

- Ignoring local deposit regulations and platform return timelines.

The Simplest Counterargument

Plenty of owners run successfully with almost none of this — a modest hold, good guests, and a relaxed attitude toward the occasional broken glass. Deposits create friction and disputes; waivers add a cost to every booking; protection products add another vendor and another set of terms. For a low-exposure property with careful guests, all of it can feel like overhead in search of a problem.

That objection holds for some properties. The administrative weight of deposits and waivers is real, and the right amount of it scales with your turnover, your loss history, and how much of your business runs off-platform.

What Still Matters

Not every owner needs a deposit, a waiver, and a protection product. Many do fine with one well-run tool, or with prevention plus insurance and a tolerance for absorbing small losses.

But every owner should know which tool — if any — actually protects each booking channel, what it covers, what it costs in money or friction, and exactly where its ceiling hands off to the insurance layer. These are not insurance, and they're not a substitute for building a safe, durable property in the first place. They're the middle of the stack: the everyday money tools for the ordinary damage prevention didn't catch and insurance shouldn't have to.

The deposit you can prove and the waiver you understand are worth more than the larger one you can't.

Editorial notice

This guide is educational only. It is not legal, insurance, tax, or financial advice. Security deposits, damage waivers, and damage-protection products are governed by a mix of booking-platform terms, provider contracts, and local laws that vary significantly by jurisdiction, property type, and booking model — including rules on how much may be held, how funds must be handled, and how and when they must be returned. Every owner should confirm current platform terms and applicable local rules, and consult licensed professionals for their specific situation. ASTRO does not sell, hold, administer, or endorse any deposit, waiver, or protection product, and names no provider as a recommendation.

Naming note: deposits, waivers, products, and policies

This guide keeps the same terminology discipline as its companions.

- A security deposit is refundable money associated with a reservation, claimable against attributable, guest-caused damage.

- A damage waiver is a typically non-refundable fee paid in exchange for coverage of accidental damage up to a limit — not a refundable hold.

- A damage-protection product may be an insurance product, a waiver, or a reimbursement service; the three are not interchangeable.

- A booking-platform damage process is a channel-specific reimbursement or resolution workflow under that platform's terms.

- Insurance policies — core property, liability, contents, and business-income coverage — are the backstop, covered in the protection stack guide, not here.

- ASTRO programs are ASTRO-side owner opportunities and platform features. Deposits, waivers, and third-party protection products are none of those.

Related owner reading

- The Safe and Durable Property — the prevention layer that reduces how often you need any of this.

- Short-Term Rental Insurance: The 5-Layer Protection Stack — the backstop for serious loss.

- All owner field guides

- Owner playbooks

- Support